Bojan Nikolic: Using and Understanding the QuantLib Addin

Interpolation in QuantLib¶

See for example [1] for a discussion of interpolation in finance. See also our QuantLib calculator for curve interpolation here http://quantpanel.bnikolic.co.uk/InterpolatedCurve.

One dimensional interpolation¶

The following interpolation types are available in the QuantLib add-in:

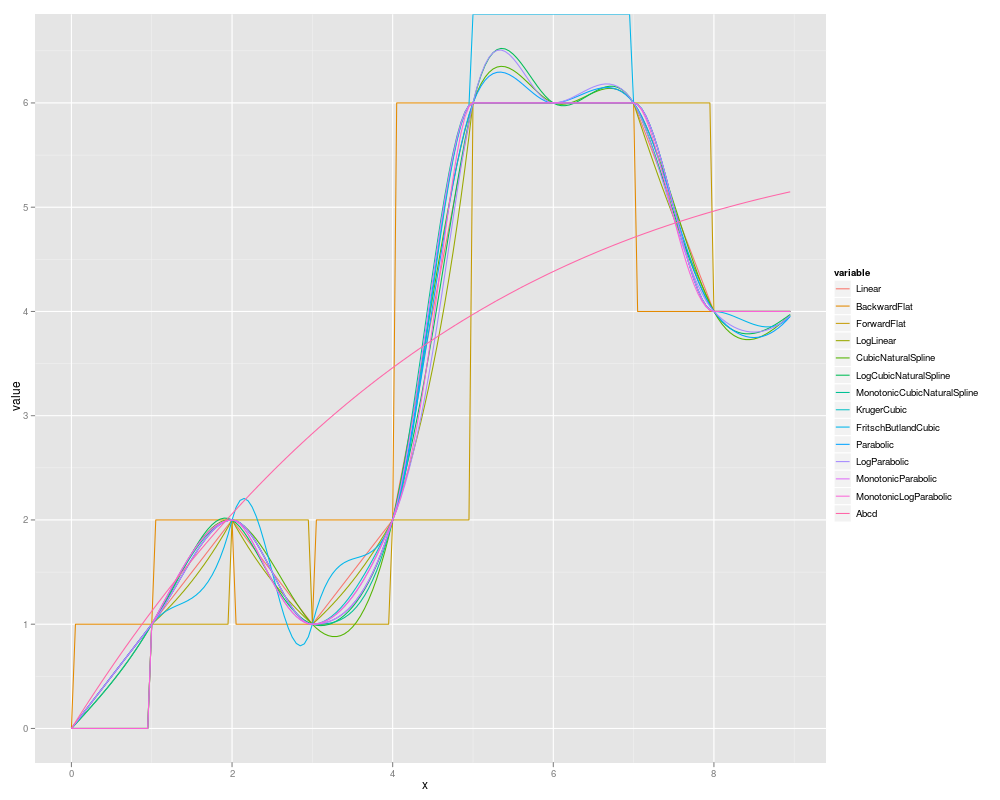

BackwardFlat

ForwardFlat

Linear

LogLinear

CubicNaturalSpline

LogCubicNaturalSpline

MonotonicCubicNaturalSpline

KrugerCubic

FritschButlandCubic

Parabolic

LogParabolic

MonotonicParabolic

MonotonicLogParabolic

Abcd

An interpolation can be constructed by calling the qlInterpolation

function and then used by calling the qlInterpolationInterpolate

function.

Below is an example plot of 10 data points interpolated using the various types of interpolation:

Two dimensional interpolation¶

The QuantLib add-in provides two types of two dimensional interpolation:

BiLinear

BiCubic

Two dimensional interpolation objects are created using the

qlInterpolation2D function and can then be used to calculate an

estimated value by using the qlInterpolation2DInterpolate function.